PropTech IT & AI Consulting

Proven IT & AI Leaders for Property Technology Companies

PropTech IT & AI Experts

PropTech occupies an unusual seat at the table: it sells technology to an industry in the middle of its own technology awakening. Buyers who once tolerated clunky software now arrive with AI expectations, security questionnaires, and real procurement teams; investors are funding the platforms with genuine data moats and passing on everything else; and a single Justice Department settlement has turned pricing algorithms into regulated artifacts. For a property-technology company, technology is not a support function; it is the company. Here, AI strategy IS IT strategy, and both of them are product strategy too.

Innovation Vista advises property-technology companies from their side of the table. Contract CIO+® places fractional CIO and CTO-caliber leadership inside the business, CIO IQ® keeps seasoned counsel on call, and our AI strategy practice helps you decide what to ship and what to run. The guidance is independent and vendor-neutral, with no commissions or resale margins anywhere in it, and it draws on a network of 450+ consultants matched by sector: leaders who have built and scaled software companies, and who have also run technology for the owners and operators you sell to.

That second point matters, because our proptech work connects directly to our residential real estate and commercial real estate IT & AI consulting practices; we understand both sides of your market because we advise both sides of it. Our home turf is the mid-market: growth-stage platforms, established niche vendors, and PE-backed proptech portfolios. Engagements usually open with an IT & AI Assessment, a few weeks of work that shows founders, boards, and investors exactly where the architecture, the data, and the AI readiness stand.

State of Innovation in PropTech

Our 2026 Summary of Innovation in the PropTech sector

PropTech’s 2026 runs on a paradox: more capital is flowing into the sector than at any point in years, and the bar for earning any of it has never been higher. Understanding both halves of that sentence is the strategic work of the moment.

The money came back selective. Venture investment in property technology surged in 2025, up by roughly two-thirds year over year, and the pace has continued into 2026. But the distribution tells the real story: a large majority of that capital went to a small group of big financings, while a long tail of undifferentiated companies struggles to raise past seed. AI-native platforms, built around proprietary data pipelines, are growing investment at nearly twice the rate of conventional proptech; bolting a chatbot onto legacy software no longer counts. The market now sorts companies into platforms with durable data moats and everyone else, and it is consolidating the second group into the first.

Algorithms just became regulated artifacts. The Justice Department’s settlement with RealPage restricts how pricing recommendations may work: no real-time nonpublic competitor data, training data aged at least a year, auto-accept functions redesigned, and a court-appointed monitor with code-level access for years to come. Whatever one thinks of the case, the message to every proptech company is unambiguous: if your product makes consequential recommendations, its governance, transparency, and auditability are now product features, and buyers’ counsel will ask about them.

Agents are entering the workflow. Leasing assistants that carry a prospect from inquiry to signed lease, agents that triage maintenance, models that read rent rolls and underwrite deals; the agentic wave is arriving through both the platform giants and a crop of specialist vendors. Notably, the big platforms are opening to third-party agents rather than walling them out, which creates room for focused products that do one workflow exceptionally well. The catch is integration gravity: in most segments, viability still hinges on how deeply and reliably you can read from and write to the systems of record your customers already run.

Your buyers grew up. Owners and operators now run real procurement: security certifications like SOC 2, data-ownership and exit terms, integration depth, references, and increasingly, questions about how your AI works and what it was trained on. The proptech companies winning enterprise deals treat that diligence gauntlet as a sales asset they prepared for years earlier, not a fire drill.

The thread through all of it: in this sector the moat is data plus distribution, and both are earned with architecture. The companies that own clean, well-governed data pipelines and integrate deeply where it counts are compounding; the ones that deferred those decisions are discovering that AI amplifies architectural debt as efficiently as it amplifies everything else.

The Difference Between Using AI and Shipping It

Why a PropTech IT & AI Assessment Pays for Itself First

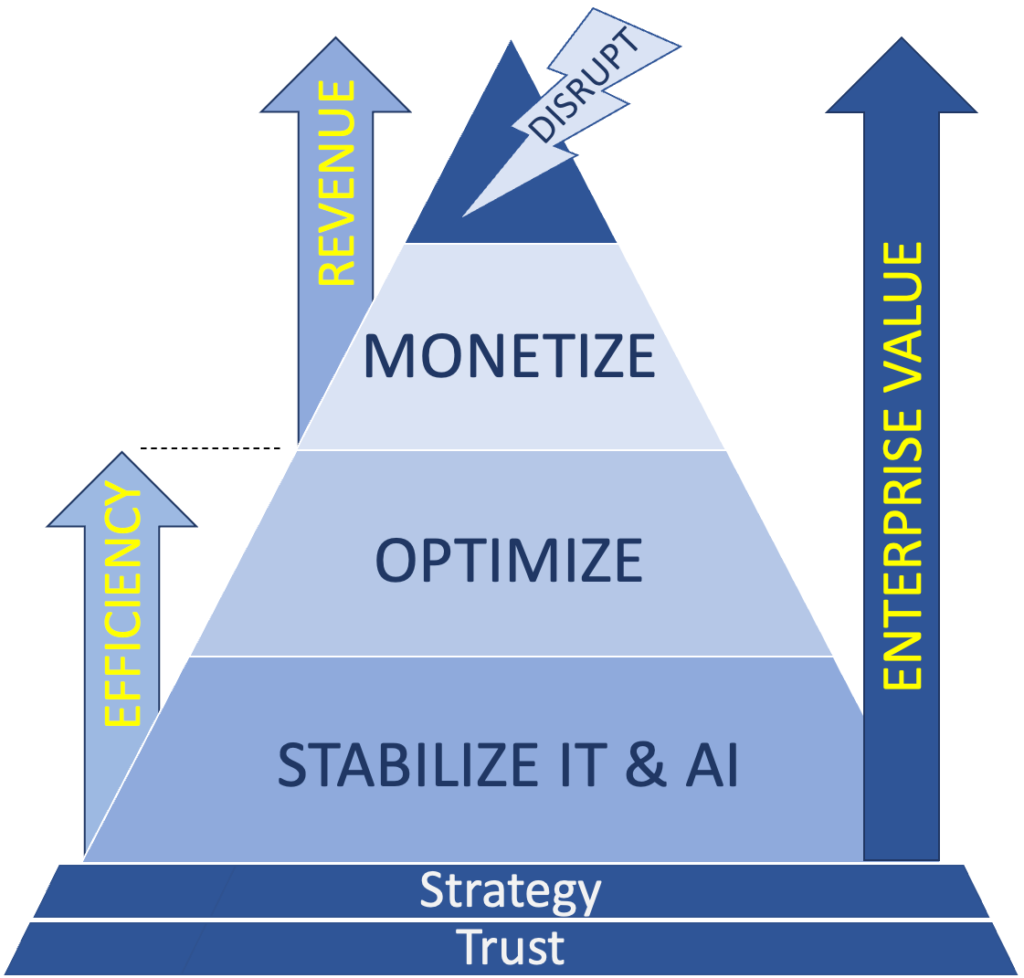

Inside most proptech companies, AI is everywhere and nowhere. Engineers code with copilots, support drafts replies with assistants, marketing generates campaigns; useful, but none of it is the business. What moves a proptech company is production AI: intelligence shipped inside the product and run inside operations, leasing agents customers can rely on, models that read rent rolls and inspect units, underwriting that survives an auditor, anomaly detection your largest client trusts at two in the morning. The distance between everyday AI use and production AI is exactly the distance between the two tiers of today’s funding market, and it is crossed with architecture and governance, not enthusiasm.

Our IT & AI Assessment measures that distance for a proptech company in weeks. It examines what investors, acquirers, and enterprise buyers will examine sooner or later: whether your data architecture actually constitutes a moat or just a warehouse; how deep and resilient your integrations to the industry’s systems of record really are; whether security, compliance, and AI-governance posture would clear an enterprise procurement review or an acquirer’s diligence; where your cloud economics will bend or break as you scale; and which one or two production AI capabilities would most strengthen your competitive position given your stage. The deliverable is a sequenced, board-ready plan tied to valuation and revenue, not a tooling list.

The bottom line: sometimes the honest finding is that the foundation under the product needs work before the next AI feature ships, and hearing that before a funding round or an enterprise deal is worth multiples of the assessment. More often it is a short, concrete agenda: the pipeline to harden, the integration to deepen, the governance to document, and the production AI move that wins deals. In proptech, the moat is built in the architecture long before it shows up in the pitch deck.