Banking IT & AI Consulting

Proven IT & AI Leaders with Track Records in Banking

Banking IT & AI Experts

In banking, technology decisions never stay in the IT department. The core processes every deposit, the mobile app is the busiest branch, and the examiner’s questions about your models arrive whether or not the answers are ready. Community banks, regional institutions, and bank holding companies are expected to deliver fintech-grade experiences on mid-market budgets while proving that every system, model, and vendor is under control. In 2026 that pressure has a simple corollary: AI strategy IS IT strategy, and a bank cannot get one right without the other.

Innovation Vista exists for exactly this kind of decision-making. We bring fractional and virtual CIO leadership to banks through our Contract CIO+® service, ongoing counsel through CIO IQ®, and dedicated AI strategy guidance, all of it independent and vendor-neutral; we sell no hardware, resell no software, and accept no referral fees from vendors we might recommend. Our network of 450+ consultants is matched to engagements by sector, so the people shaping a bank’s technology agenda have run technology inside banks; our founder served as CIO for two subsidiaries of money-center banks before building the firm.

Banking sits at the center of our broader financial services IT & AI consulting practice, and mid-market institutions, from community banks to multi-bank holding companies, are the clients we are built for. Most engagements begin with a focused IT & AI Assessment: a few weeks of work that tells you exactly where your technology estate and your AI readiness stand before you commit to anything larger.

State of Innovation in Banking

Our 2026 Summary of Innovation in the Banking sector

Banking’s AI conversation has changed character over the past eighteen months. The question inside bank leadership teams is no longer whether to use AI; it is why the pilots have not become production. A majority of banking executives now expect AI agents to be embedded in risk, compliance, fraud monitoring, and credit operations within the next few years, and every layer of the vendor stack is shipping agentic capability. Yet research keeps finding that only about one organization in ten has agentic AI genuinely running in production, and banks attempting to scale beyond isolated programs routinely stall. The separation happening in banking right now is at the production line, not the pilot line.

The rulebook is being rewritten mid-flight. In April 2026 the OCC, Federal Reserve, and FDIC issued their first major revision of model risk management guidance since 2011, shifting to a principles-based approach scaled to each institution’s size and complexity. Notably, the agencies placed generative and agentic AI outside the scope of that guidance and promised separate AI guidance to come; banks are deploying AI faster than the framework that will eventually judge it. That makes internal governance, documentation, and explainability the only safe harbor an institution can build today.

Open banking gave banks whiplash instead of a mandate. The CFPB’s Section 1033 data-sharing rule was stayed in court and is being rewritten, with compliance deadlines suspended while that happens. The strategic question has flipped: data openness is no longer something Washington requires; it is something customers reward. Banks that built API and data-sharing infrastructure for the rule now get to decide how much of it to deploy as a competitive weapon rather than carry as a compliance cost.

Instant payments crossed from experiment to expectation. Roughly 1,500 institutions now participate in FedNow, the overwhelming majority of them community-scale, and the RTP network is approaching half a trillion dollars in quarterly volume; thousands of banks nevertheless remain receive-only or entirely on the sidelines. Real-time rails change far more than settlement speed. Fraud decisions that once had a day now have a second, liquidity becomes an intraday discipline, and commercial customers increasingly treat instant payment capability as table stakes when choosing where to bank.

Fraud is now an AI-versus-AI contest. Deloitte projects that generative AI could push US fraud losses toward $40 billion by 2027, and banks sit at the leading edge: synthetic identities that sail through legacy onboarding, deepfaked voices aimed at wire desks and call centers, and AI-polished variations on the oldest banking crime of all, check fraud. Identity and verification stacks designed five years ago were built for a different adversary, and rebuilding them has become a 2026 budget line at institutions of every size.

Underneath all of it sits the core. A small number of core providers process for the large majority of US depository institutions, and for many banks the practical AI roadmap is whatever the core vendor ships next. That dependency is the quiet strategic question of 2026. Core conversion and renegotiation activity is running at levels the vendors themselves describe as record-setting, and the more progressive institutions are building around the core rather than waiting on it, putting data, digital channels, and AI capability in layers they control. The pattern across every trend this year is the same: advantage belongs to banks that can move new technology into production under full regulatory scrutiny, and that is a foundation question before it is a model question.

From Citizen AI to Production AI

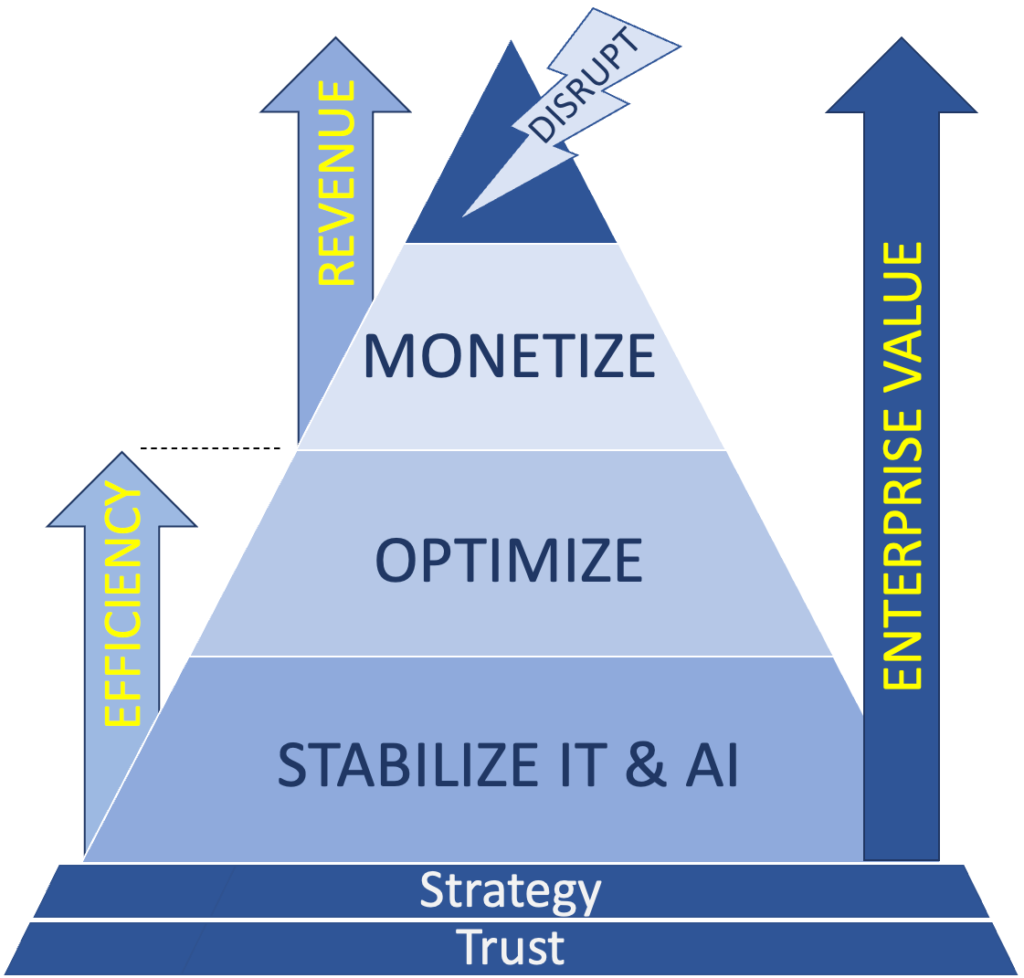

Why a Banking IT & AI Assessment Comes First

Walk through any bank today and AI is already at work: a lender drafting credit memos with a chatbot, marketing generating campaign copy, an analyst summarizing call reports. That is citizen AI, individual employees using general-purpose tools, and it is worth encouraging; but it is not where competitive advantage lives. Production AI is different in kind: models and agents embedded in the bank’s actual operations, in underwriting, onboarding, fraud interdiction, and servicing, wired into the core and the data estate and governed well enough to survive an exam. The distance between scattered citizen AI and production AI is precisely where banks will separate over the next three years, and crossing it is a readiness problem before it is a technology problem.

Our IT & AI Assessment gives a bank that readiness picture in weeks, not quarters. For a banking client it examines the things that determine whether production AI is even possible: how cleanly data moves among the core, lending systems, digital channels, and CRM; how much of the roadmap is hostage to a core contract and what leverage exists at renewal; whether model governance and documentation would satisfy an examiner applying the agencies’ new guidance; how the fraud and identity stack holds up against AI-generated attacks; and where instant payments fit the bank’s deposit and treasury strategy. It ends in plain-language recommendations sequenced by risk and return, not a software shortlist.

The bottom line: the honest output of an assessment is sometimes “not yet”; far better to learn that in a report than in production with a regulator watching. More often the output is a specific, fundable path: what to stabilize, what to fix in the data, and which one or two production AI use cases your bank is positioned to win first. Readiness, not enthusiasm, is what turns AI from an expense into market share.