Software and services vendors are quietly running one of the cleanest arbitrage trades in recent memory, and most mid-market buyers haven’t noticed.

The mechanism is simple. AI has compressed vendor cost-of-goods (via the “AI Dividend“) on a wide range of work by a meaningful percentage; in some categories, the compression is half or more. The pricing anchors clients use to evaluate vendor proposals haven’t moved correspondingly. Vendors sitting between the new low input cost and the old high output price are capturing the spread, often for the entire duration of multi-year renewals. The trade isn’t malicious; it’s rational. Most vendors aren’t even framing it as arbitrage internally. They’re just observing that their margins have improved and structuring renewals to preserve the improvement.

The trade is also time-bounded. Buyer awareness is catching up, AI-native challengers are entering markets with lower price points, and the next renewal cycle will close some of the spread regardless of what individual buyers do. The question for mid-market firms entering 2026 vendor renewals isn’t whether the arbitrage exists; it does. The question is whether the firm is going to be on the wrong side of the trade for another two or three years, or whether it’s going to restructure the relationship now while the spread is still wide enough to share.

The arbitrage isn’t universal; it lives where two variables intersect

The first mistake mid-market buyers make is assuming the AI arbitrage applies to every vendor relationship equally. It doesn’t. The arbitrage exists only in work where two specific conditions hold:

AI can execute the delivery, not just accelerate the overhead. This depends primarily on training data availability. Work patterns that exist in the AI training corpus are work patterns AI can substantially execute; work patterns that don’t exist there are work patterns AI can only support around the edges. The first kind of work has experienced delivery-cost compression; the second hasn’t.

The work isn’t firm-specific enough to require internal context. Some work is structurally portable: a vendor can run it across many clients without much customization, and the productivity gains accrue cleanly to the vendor’s margin. Other work compounds on accumulated internal knowledge: data, customer relationships, internal politics, competitive position. The first kind belongs outside the firm; the second belongs inside.

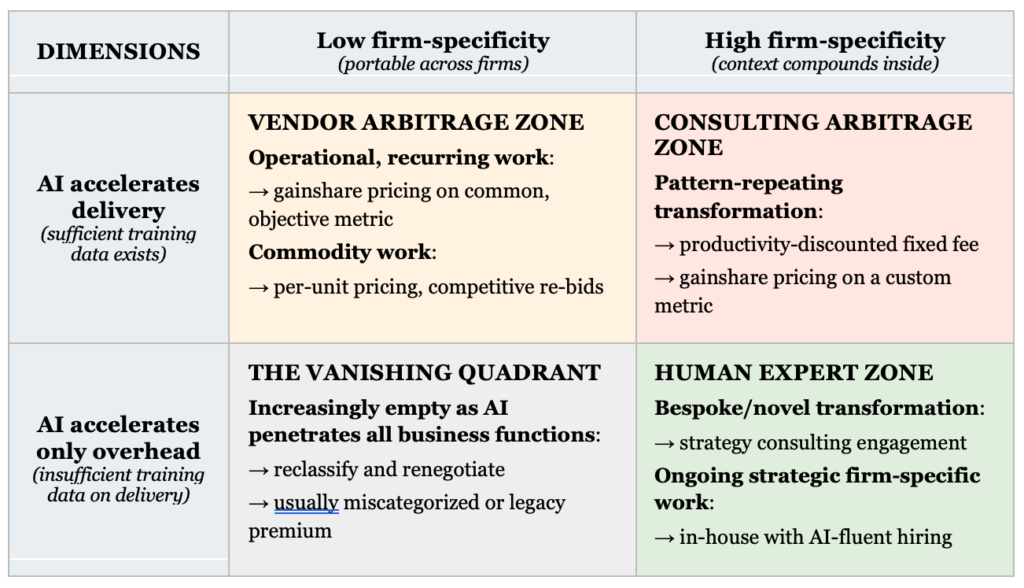

These two variables, taken together, produce a four-quadrant map of where AI arbitrage actually exists, where it doesn’t, and where the partnership conversation should focus.

The AI Arbitrage map

Each quadrant calls for a different sourcing strategy and a different flavor of partnership.

Top-left: the vendor arbitrage zone

AI executes the work. The work isn’t firm-specific. Vendors capture meaningful productivity gains across their portfolio, but those gains aren’t flowing to client invoices. This quadrant contains most of the AI arbitrage that affects mid-market buyers, and it splits into two sub-categories that warrant different treatment.

Operationally important, recurring work. Back-office processing, certain categories of analysis, ongoing technical operations, specific kinds of customer-facing support, recurring data work. The work is important enough to matter, recurring enough to scale, and scale-economic enough that vendor specialization beats in-house repetition. The partnership flavor is gainshare on a client-observable metric, structured around four components:

- A jointly designed baseline, documented with evidence from before the AI-era productivity gain was captured.

- A measurable output metric the client observes independently of vendor reporting, denominated in something that scales with the work (transactions per period, hours per output unit, processing volume per cost dollar).

- A defined share split on gains relative to baseline, with both sides understanding that the share preserves vendor margin incentive while transferring real value to the client.

- A sunset and reset clause every 18-24 months, because productivity continues to compound and the baseline that was honest in 2026 will be obsolete by 2028.

The hardest part of designing these structures isn’t the share split; it’s the baseline. Baselines set by the vendor before deployment tend to favor the vendor; baselines set by the client after seeing results tend to favor the client. The right baselines are co-designed, evidence-based, and documented in enough detail that neither side can rewrite them later.

Commodity work. Standard software licensing in non-strategic categories, generic infrastructure, routine processing services. The arbitrage exists here too, but it doesn’t need to be solved through partnership structures because vendor competition will compress price naturally as the market becomes aware of the productivity gain. The partnership flavor is simply per-outcome or per-unit pricing, with annual re-bid cycles. Clients shouldn’t waste negotiation capital trying to design gainshare structures here; they should run competitive bids and let the market do the work.

The distinction between these two sub-categories matters because the negotiation effort required for gainshare is substantial and should be reserved for work where the spread is large and the relationship is strategic enough to warrant the design work.

Top-right: the consulting arbitrage zone

AI executes the work. The work has enough firm-specificity that it lives in consulting rather than in pure productized vendor services. But the consulting pattern itself exists in the training data.

This is the part of consulting where AI is genuinely compressing delivery cost: standard ERP rollouts, common digital transformation playbooks, routine compliance preparation, well-trodden M&A integration approaches. Sufficient training data exists for AI to meaningfully accelerate the actual delivery, not just the consultant’s overhead. Hours per outcome have dropped materially over the last 18 months for firms that have integrated AI into delivery.

For this quadrant, the arbitrage is real on the consulting side, and the right partnership flavor is a fixed-fee engagement with an explicit productivity discount, or alternatively a shared-upside structure tied to the transformation outcome. Either acknowledges that the work costs less to deliver than it did 24 months ago and shares some of the savings with the client. Firms accepting AI-era engagements at pre-AI fee structures should expect their consultants to be running healthy margins on the spread.

This is also the quadrant where the largest consulting firms are most exposed. Big Four engagements rely heavily on pattern recognition against well-documented playbooks; that’s exactly the work AI compresses fastest. Their fee structures will eventually have to reflect productivity gains, but most haven’t repriced yet. Clients evaluating Big Four proposals in this category should expect to see explicit AI-era discount structures by 2027.

Bottom-right: the human expert zone

AI accelerates the consultant’s or operator’s overhead, but not the delivery itself. The work has enough firm-specificity that the durable advantage compounds inside the firm or in the working relationship.

This quadrant is where mid-market firms should be focusing their strategic investment, and it’s the quadrant most consulting commentary gets wrong. Within the human expert zone, two distinct work types share the territory.

Bespoke & novel transformation work. Bespoke situations where the client’s circumstances have no clear analog in available training data. Novel competitive responses, first-time strategic pivots, complex multi-stakeholder reorganizations, situations where the diagnostic itself is the deliverable. AI helps the consultant’s research, drafting, and engagement overhead, but the core judgment work still requires accumulated pattern recognition that careers build, and that pattern recognition isn’t in any training corpus. The partnership flavor here isn’t pricing structure; it’s scope and access, meaning longer engagement durations, clearer access to firm leadership, and expectations of strategic continuity rather than transactional deliverables.

Ongoing strategic firm-specific work. Continuous work that depends on accumulated firm context: knowledge of the company’s data, customers, history, internal politics, competitive position. The work is continuous rather than episodic, which matches the duration profile of employment rather than engagement. The partnership flavor here is internal: AI-fluent hiring with the right blend of domain expertise. The relevant 2026 question isn’t whether to source internally; it’s how to recruit AI-fluent operators when the labor market for them is tight and slow.

What the pricing conversation usually misses about the human expert zone is the asymmetry on the value side. Novel transformation work, in particular, is precisely where the largest ROI lives for mid-market firms, often by orders of magnitude relative to pattern-rich engagements. The reason is structural. If a transformation pattern is in the AI training data, it’s also in your competitors’ AI tools. They can run the same diagnostic, generate the same recommendations, and execute the same playbook you can. The competitive advantage from pattern-rich work is real but shallow, because the half-life of the advantage is bounded by how quickly competitors can ask the same AI the same question.

Bespoke/novel work is the inverse. The transformation that has no playbook is the transformation competitors can’t copy by asking Claude or any other model what to do. Genuine strategic novelty, by definition, lives outside the training corpus. That’s where durable competitive advantage gets created in the AI era, and it’s where consulting fees buy results that aren’t available to firms that didn’t invest in the work.

There’s a misconception that this kind of work is the province of large enterprise, that mid-market firms mostly operate within well-established patterns and need to execute the standard playbooks better than their peers. The reverse is closer to true. Large enterprises operate at scales where their playbooks are visible, their analysts are well-funded, and their consulting partners have seen dozens of similar situations. The strategic problems facing mid-market firms are often more genuinely unique: tighter constraints, narrower talent pools, more dependence on specific customer relationships, more variability in competitive position, more idiosyncratic ownership structures. The bespoke quality that makes pattern-novel work expensive to source is also what makes it disproportionately available to mid-market firms relative to their enterprise counterparts.

Clients should expect to pay traditional consulting rates for pattern-novel work and should be skeptical of providers offering aggressive discounts in this quadrant; the discount usually signals that the work has been miscategorized, or that the consultant is competing on price because they lack the judgment depth to justify the fee.

Bottom-left: the vanishing quadrant

The fourth quadrant, where work is neither firm-specific nor amenable to AI execution, is increasingly empty. AI is touching almost everything that’s broadly applicable, and the work that remains genuinely AI-resistant tends to be firm-specific. If a buyer finds themselves paying for services that fall into this quadrant, the most likely explanation is one of these three (in all three cases, the action is the same: re-examine the relationship, reclassify the work, and renegotiate accordingly):

- The work has been miscategorized; it’s actually in the top-left and the vendor has obscured the AI exposure.

- The buyer is paying a brand premium for legacy reasons that no longer reflect underlying economics.

- The work category itself is on a trajectory toward AI tractability, and the current contract is locking in pricing ahead of the inevitable compression.

Why the diagonal matters strategically

The map has a diagonal that’s worth naming explicitly. Moving from the top-left (operationally efficient at portable, AI-tractable work) toward the bottom-right (human expert, AI-resistant, firm-specific) is moving from “compete on price” to “build durable advantage.”

This isn’t just a map of how to source vendor work. It’s a map of where the firm itself should be investing capability development. The strategic question every mid-market CEO and CFO should be asking right now is: which quadrant does our own value creation live in, and is it the right quadrant for the next five years?

Firms whose competitive advantage lives in the top-left quadrant (operationally efficient at portable tasks) are exposed; AI is eroding the moat by giving every competitor the same productivity tools. Firms whose advantage lives in the top-right quadrant (consulting-style application of known patterns) are similarly exposed; the patterns are commoditizing. Firms whose advantage lives in the bottom-right quadrant (genuinely firm-specific judgment, novel problem-solving, accumulated context) are protected from near-term AI disruption, but only if they continue to invest in the protection.

The diagonal isn’t a static map; it’s a vector. Strategic investment should be pulling the firm’s value creation toward the bottom-right, away from the commodity corner.

Where this lands operationally: the contract restructure exercise discussed in the top-left and top-right quadrants is the defensive move. It’s reclaiming gains that are leaking to vendors. The investment in firm-specific capability, pattern-novel strategic work, and AI-fluent in-house hiring is the offensive move. It’s building durable advantage that competitors can’t replicate by asking Claude what to do.

Sophisticated mid-market firms in 2026 will run both moves simultaneously. Most will only run one, and most of those will choose the defensive one because it’s easier to justify on a year-over-year basis. The firms that capture the most durable advantage will be the ones that use the savings from the defensive move to fund the offensive one.

The map shifts

One additional dynamic worth holding onto. The line between AI-executable and AI-overhead-only isn’t static; it moves as training corpora grow. Work that’s genuinely bespoke in 2026 may become tractable for AI by 2028 as more examples accumulate. The categorization is therefore not a one-time exercise. Vendor relationships and consulting engagements should be re-evaluated periodically, with the expectation that work shifting from the human expert zone to the arbitrage zones should trigger renegotiation of the underlying fee structure.

The right cadence for this re-evaluation is roughly the same as the sunset clauses recommended for top-left partnerships: 18-24 months. Firms that build this rhythm into their vendor management practice will stay ahead of the moving boundary; firms that don’t will discover, periodically and expensively, that work they’ve been paying premium rates for has become commoditized while their contract structures haven’t caught up.

The firm-specificity axis is more stable, but it isn’t immovable either. As AI tools become better at incorporating firm-specific context through customization, fine-tuning, retrieval, and agentic memory, the cost of replicating firm-specific work outside the firm gradually declines. The human expert zone narrows over time. The most durable strategic positions are the ones whose firm-specificity comes from genuinely unique combinations of context that don’t exist anywhere else, not just from accumulated familiarity.

Honesty about consulting

The arbitrage dynamic applies to consulting itself, asymmetrically. Top-right consulting work (pattern-repeating transformation) is exactly the category where AI compresses delivery cost most, and consulting fees in that category should reflect that compression. Firms hiring consultants for standard transformations, common implementations, or well-trodden methodologies should expect to see AI-era pricing structures in the RFP responses, and should be skeptical of providers who quote pre-AI fee levels without explanation.

Bottom-right consulting work (bespoke/novel transformation) is the asymmetric exception. Here, AI accelerates the consultant’s overhead but not the delivery itself; the consultant’s accumulated judgment is the product, and that product isn’t getting cheaper to produce because the underlying pattern recognition still requires human experience. Firms should expect traditional pricing for genuinely bespoke strategic work, and providers offering aggressive discounts in this category are usually either mis-categorizing the work or competing on price because they lack the judgment depth to justify the fee.

The honest test is whether the consultant can explain which quadrant the work falls into and why. Consultants who pretend the map doesn’t exist, or who treat all their work as bottom-right to preserve premium pricing, are running a quieter version of the same arbitrage this article is highlighting.

What to do next

The categorization itself is the highest-leverage exercise. Most mid-market firms will discover, on serious inspection, that their vendor and capability spend is currently miscategorized in at least two or three significant relationships: work in the top-left quadrant being treated as bottom-left commodity (capturing none of the AI gain); work in the bottom-right being outsourced when it should be in-house; work in the top-right being paid at pre-AI rates because nobody asked the right question in the RFP.

Each situation is unique. The metric that worked for one client in the top-left quadrant doesn’t translate directly to another. The pattern-rich versus pattern-novel split in the top-right and bottom-right depends on the specific consulting work and the maturity of training data in that domain. The right partnership structures emerge from the diagnostic, not from a template.

But the diagnostic is reliably high-ROI. Across mid-market firms running this exercise in 2026, the contract restructure work is consistently the highest-leverage single move available, both because the spreads are still wide and because most competitors haven’t done the analysis yet. Firms that move first capture the gain; firms that wait participate in the compression after the market has already priced it in.

The window won’t stay open indefinitely. The arbitrage exists because buyer awareness lags vendor productivity. Closing the lag is what this article is about.